They pick assets they like, split the capital equally, and call it diversified. Equal weight is fine as a starting point, it’s simple and beats many complex approaches.

But here’s the reality: several lines of code can unlock 200+ basis points of annual alpha by optimizing how you allocate risk, not just capital.

This article examines three systematic portfolio optimization methods. Each offers a distinct mathematical framework for balancing risk and return. Test all three before settling on equal weight.

No hunches. No leaving money on the table. Just three proven allocation engines you can implement this weekend.

Return Potential: ★★★☆☆

Ease Of Adoption: ★★★☆☆

Drawdown Protection: ★★★☆☆

🆘 Common Problems

Equal weight portfolios work, but most traders stop there.

They assume simplicity equals optimality.

It doesn’t. Research shows equal weight portfolios often outperform cap-weighted benchmarks by 100-270 basis points annually [1], but optimized approaches push that edge even further. You’re leaving the money on the table by not testing alternatives.

The real issues with stopping at equal weight:

Hidden Concentration: Your 25% allocation to crypto carries 60% of your portfolio risk because of extreme volatility. Equal capital ≠ equal risk contribution

Suboptimal Risk-Return: Equal weight ignores the correlation structure between assets, missing opportunities to reduce volatility without sacrificing returns

No Adaptation: Markets change but your 1/N split stays static, failing to respond when asset relationships shift during crises

Here’s what’s frustrating: implementing proper optimization takes several lines of Python, maybe an afternoon of work, yet most traders never bother.

The three methods below let you test whether equal weight is genuinely optimal for your universe, or whether you’re sacrificing 20-30% of potential Sharpe ratio by skipping optimization.

🚨 Don’t Leave Your Money On The Table! Get The Code For Portfolio Optimization To Boost Your Risk-Based Return!

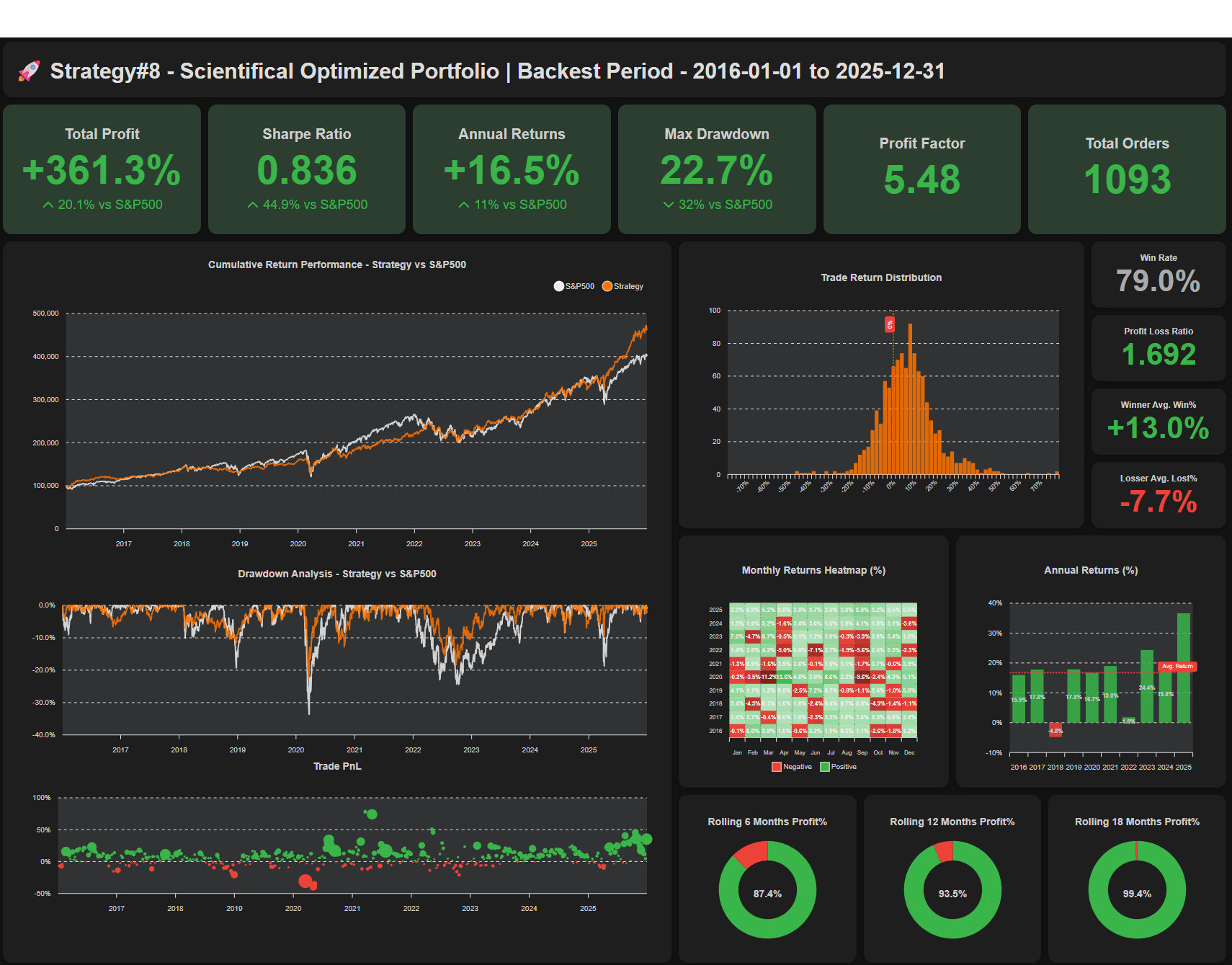

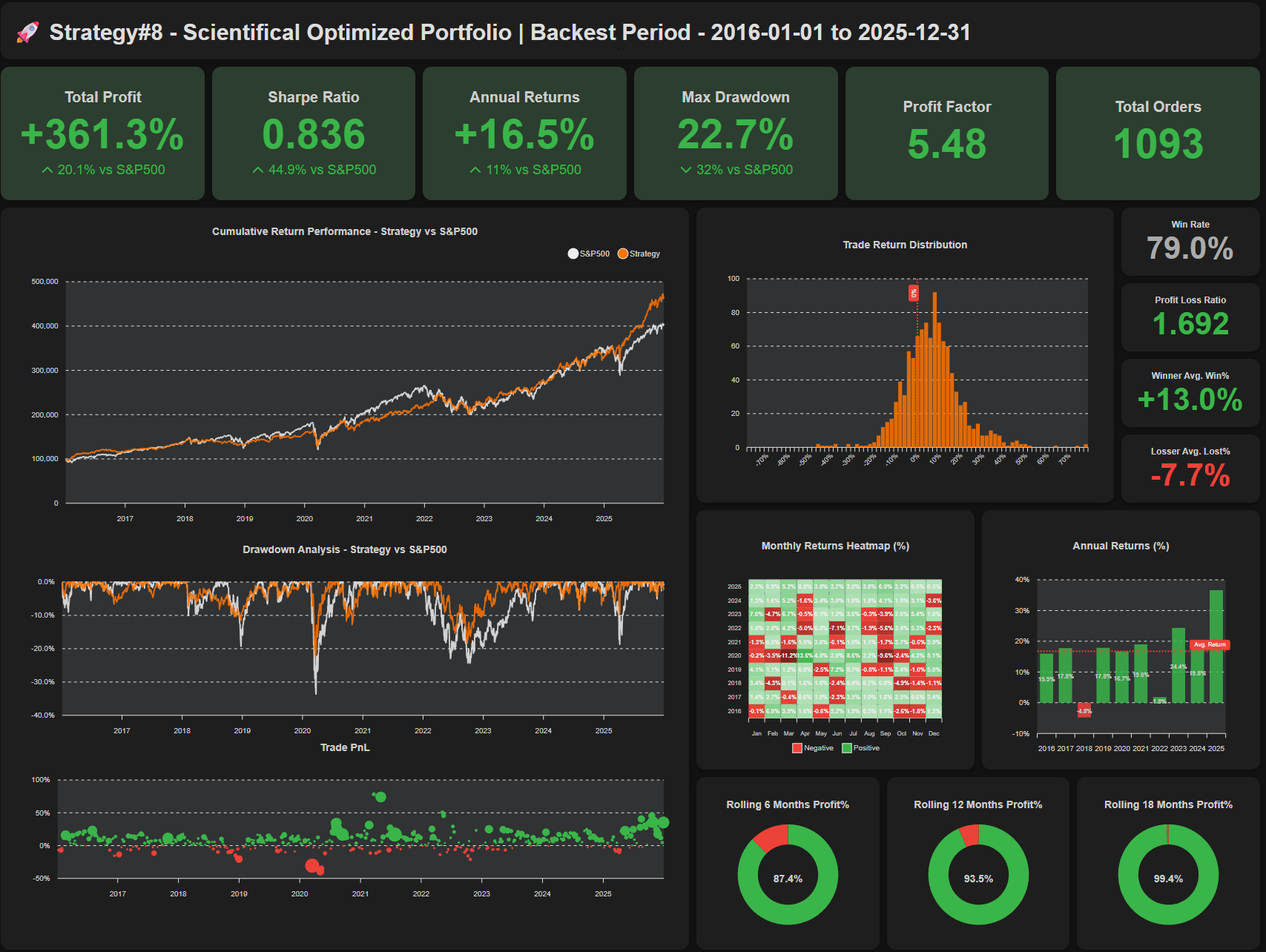

Choose the right optimization, risk-based return improved dramatically. e.g. our sample portfolio

Sharpe Ratio: 0.687 → 0.836 (✅Improved 22% )

Max Drawdown: -33.3% → -22.7% (✅Improved 32% )

Paid content to unlock the followings:

Details on the optimization setup & financial instrument used

The full optimization statistics

Source codes (in Python) for the 3 ways of optimization

Source code (In Python - QuantConnect) for optimized strategy

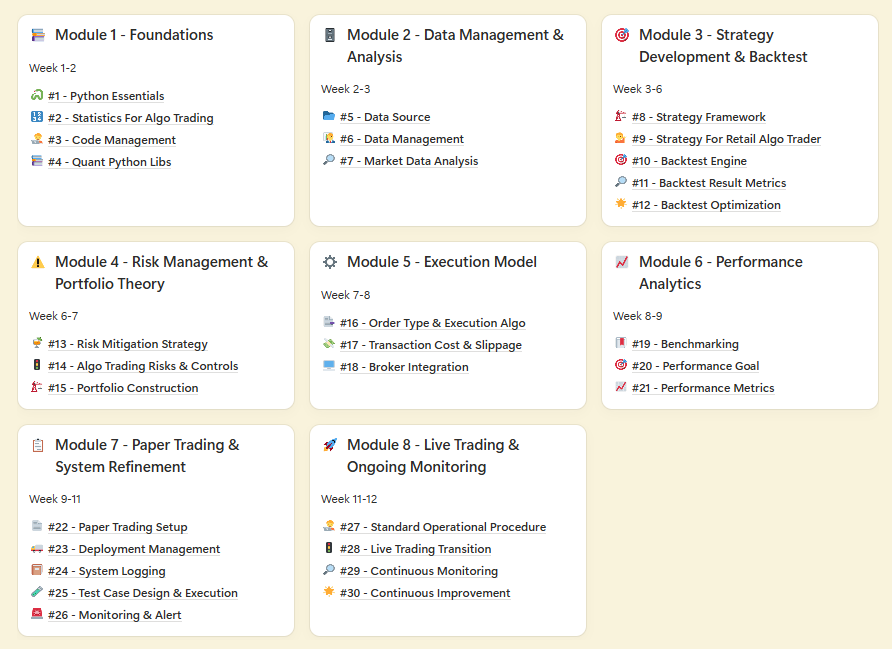

BONUS For Paid Member ONLY - “Champion’s Fast Lane Playbook: Master Algo Trading in 12 Weeks” - My 8 modules self-study guides and notes for building a winning strategy.