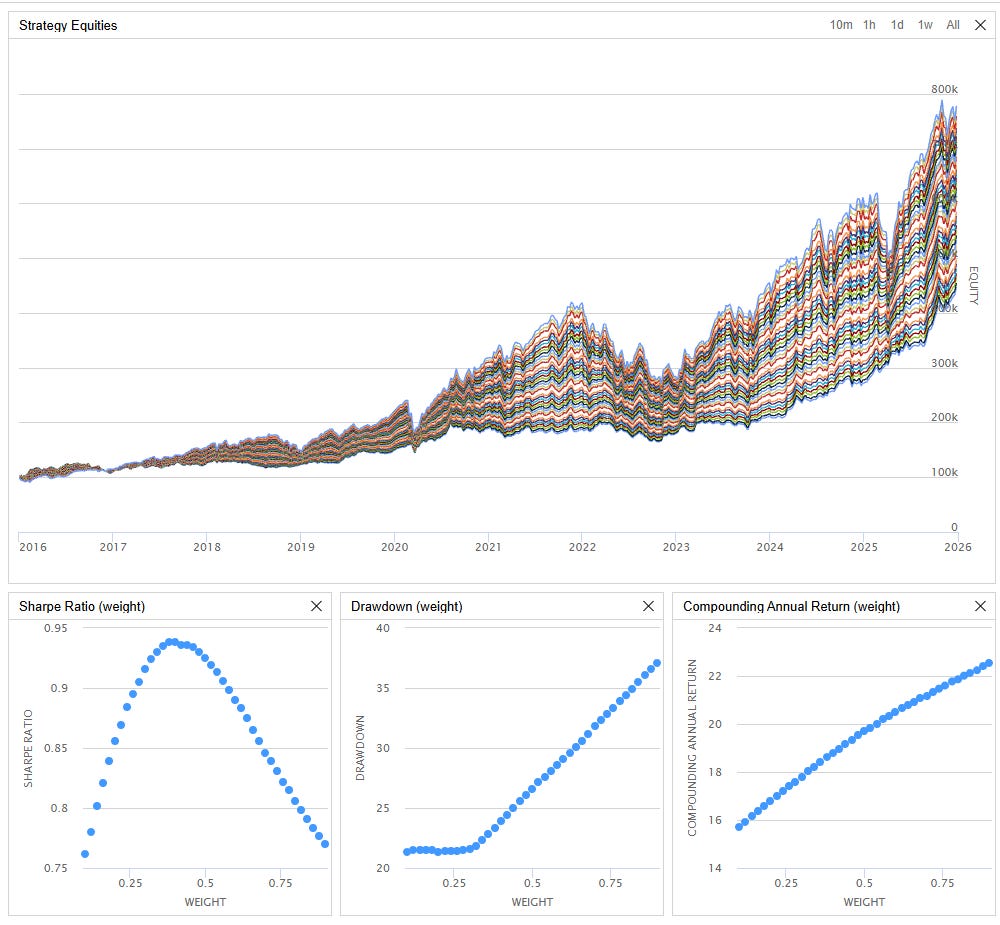

Most traders think a good backtest means they’ve found gold. They try to find out the optimized parameters by trying all combinations (like the chart above), and pick the best parameters to go live.

But backtests lie. They whisper sweet promises of 60% annual returns, then collapse in live trading.

Why?

Because fitting a strategy to all available data is like taking an exam with the answer key in your lap.

For details on why Backtest can’t be trusted, check my post below:

Walk-forward testing solves this. It simulates real-world implementation by forcing your strategy to make decisions using only data that would have been available at that moment. No future peeking. No parameter tweaking with perfect hindsight.

🆘 Common Problems

Most systematic traders fall into the same trap.

They optimize.

They backtest a strategy across 10 years of data, tweak parameters until performance looks pristine, then wonder why live trading bleeds capital within weeks.

This creates three lethal issues:

Overfitting: Parameters are tuned to historical noise rather than genuine market structure, producing strategies that memorize the past but can’t predict the future.

False Confidence: Traditional backtesting dramatically underestimates risk and overestimates returns because it tests on data the strategy was already optimized for.

Zero Adaptability: Markets evolve, trends shift, volatility regimes change but static backtests assume tomorrow looks like yesterday.

The result? Strategies that look brilliant on paper but crumble under live market conditions.

You need a testing methodology that mirrors how you’ll actually trade: making decisions in real time, with incomplete information, and adapting as markets change.

🚨 Don’t Blow Up Your Account By Launching A Overfitted BackTest Strategy Live!

Unlock the step-by-step guide to optimize your backtest WITHOUT overfitting by walk-forward testing.

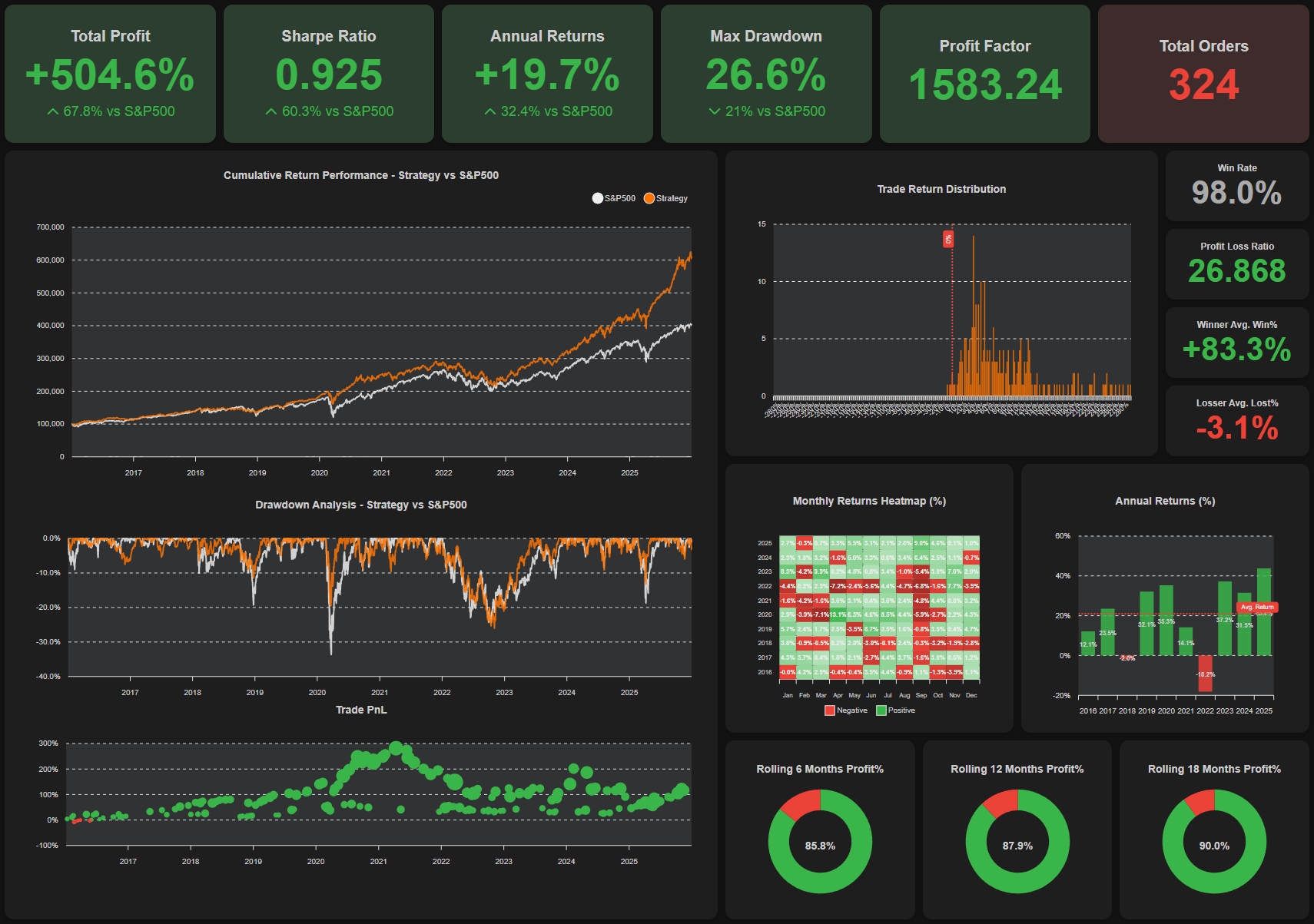

At the end of the walkthrough, you will know why 50/50 of two assets in our last strategy (+19.7% CAGR & -26.6% Max Drawdown) sharing is optimized without overfitting.

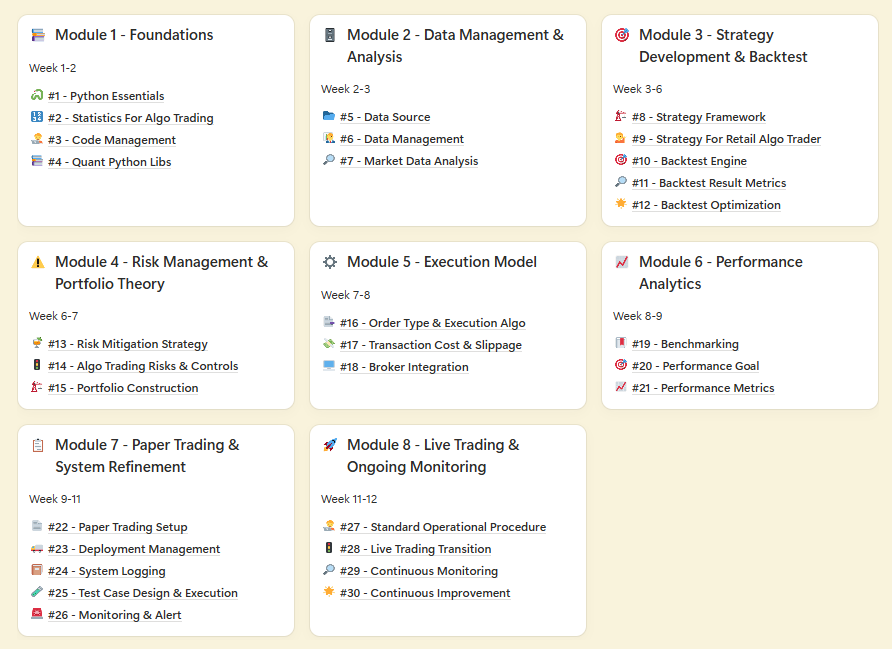

🎁 BONUS For Paid Member ONLY - “Champion’s Fast Lane Playbook: Master Algo Trading in 12 Weeks” - My 8 modules self-study guides and notes for building a winning strategy.