🎯Monte Carlo Simulation Strategy Validation Framework Series#1

Validate If The BackTest Result Is Too Good To Be Truth Before Forward Testing

In my previous Substack post, I pointed out that backtest result shouldn’t be overrlooked.

Forward testing in a live market is the ultimate stage to determine if your strategy is effective. The forward testing period should encompass:

All types of buy/sell signals generated by your trading system

Sufficient trade number to prove the system has a statistically significant edge

Various market regimes to ensure the system operates as expected

There is no strict rule for how long this period should last, it depends on your system’s trading frequency.

For example, if you’re conducting intraday trades, the forward testing period will be shorter than for a strategy involving monthly rebalancing.

Generally, for a daily strategy, forward testing should take 3-6 months.

Life is Short…We Don’t Have Too Many 6 Months of Time!

Developing a trading strategy is an iterative process. You can’t expect your first attempt to work perfectly as intended.

“Anything that can go wrong will go wrong”

Many things can go wrong, and you’ll need to fix them and conduct another round of 6 months of forward testing.

Understand that forward testing is a MUST and cannot be skipped. We need a method to filter out strategies that won’t work in advance.

That is …. Monte Carlo Simulation

Backtest shows past performance, can’t predict future uncertainties, while Monte Carlo simulations address future uncertainties .

Let me make it clear, Monte Carlo simulation is NOT a replacement for forward testing.

Instead, it serves as an additional checkpoint to assess the solidity of backtest results. While we can’t guarantee backtest results are 100% reliable, the goal is to filter out those that are unlikely to work.

The can help us to spot out those not going to work strategy, and refine before taking to a 3-6 months forward testing.

Before moving into the Monte Carlo Simulation, I listed out the questions that I need to answer to evaluate the strategy performance on top of a single snapshot of the backtesting

Is the strategy’s Sharpe ratio really better than zero, or could it just be by chance?

Does the strategy keep profitable consistently over different time periods like 1 month, 3 months, 6 months, and 12 months?

What’s the worst loss I can expect from this strategy?

Does the strategy’s risk-based returns better than just buy-and-hold S&P500 for different time frames like 1, 3, 6, and 12 months?

Will the strategy still work well if market conditions change?

This technique shuffles your list of backtested trades thousands of times to create many possible equity curves.

It helps determine if success is due to a few lucky trades i.e. outfitting. If many simulated equity curves are similar, the strategy is likely robust.

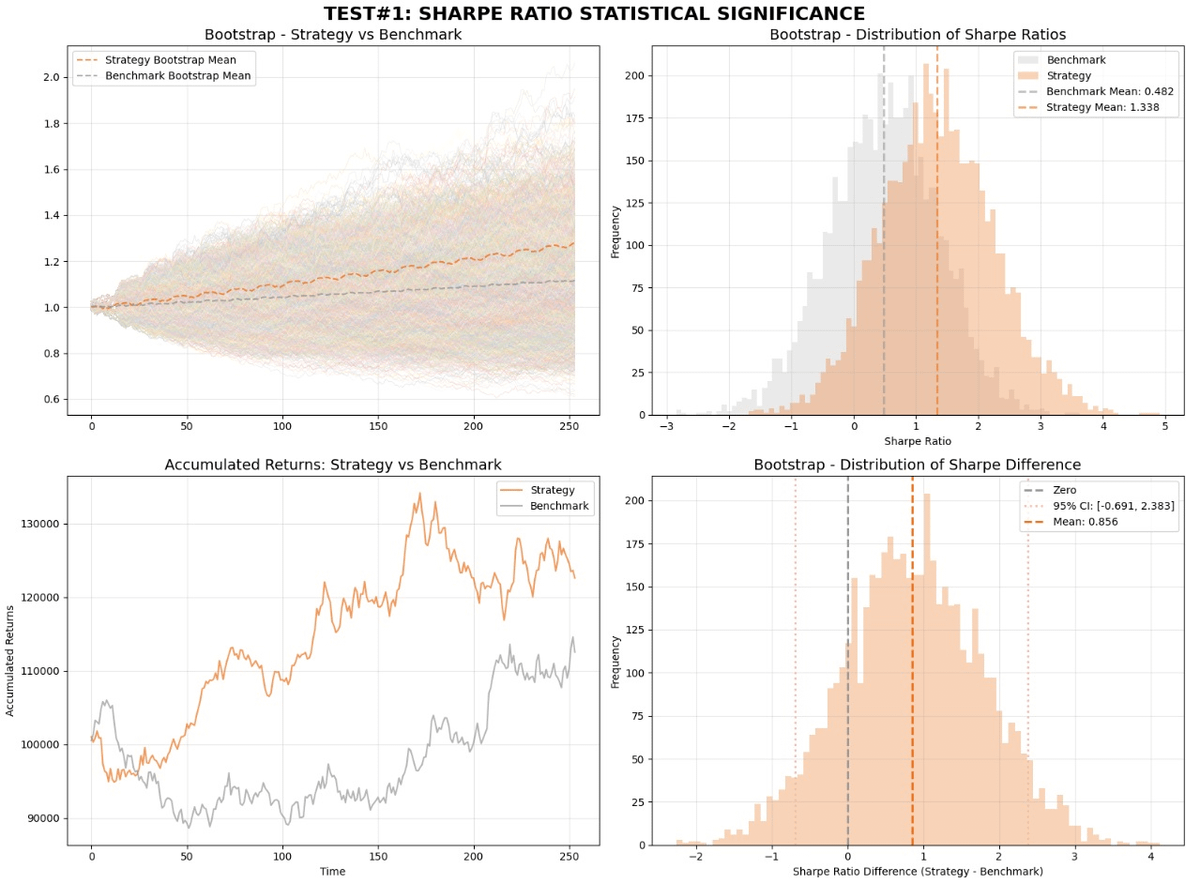

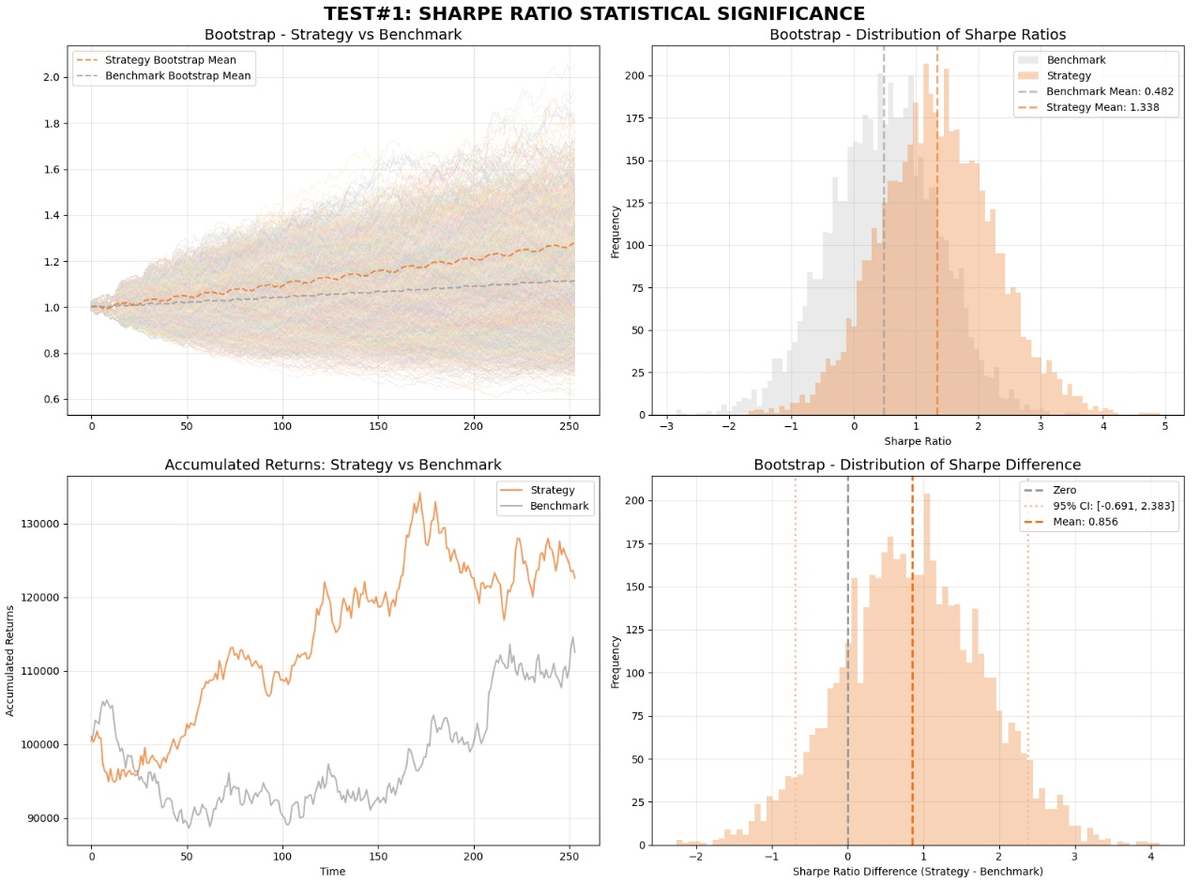

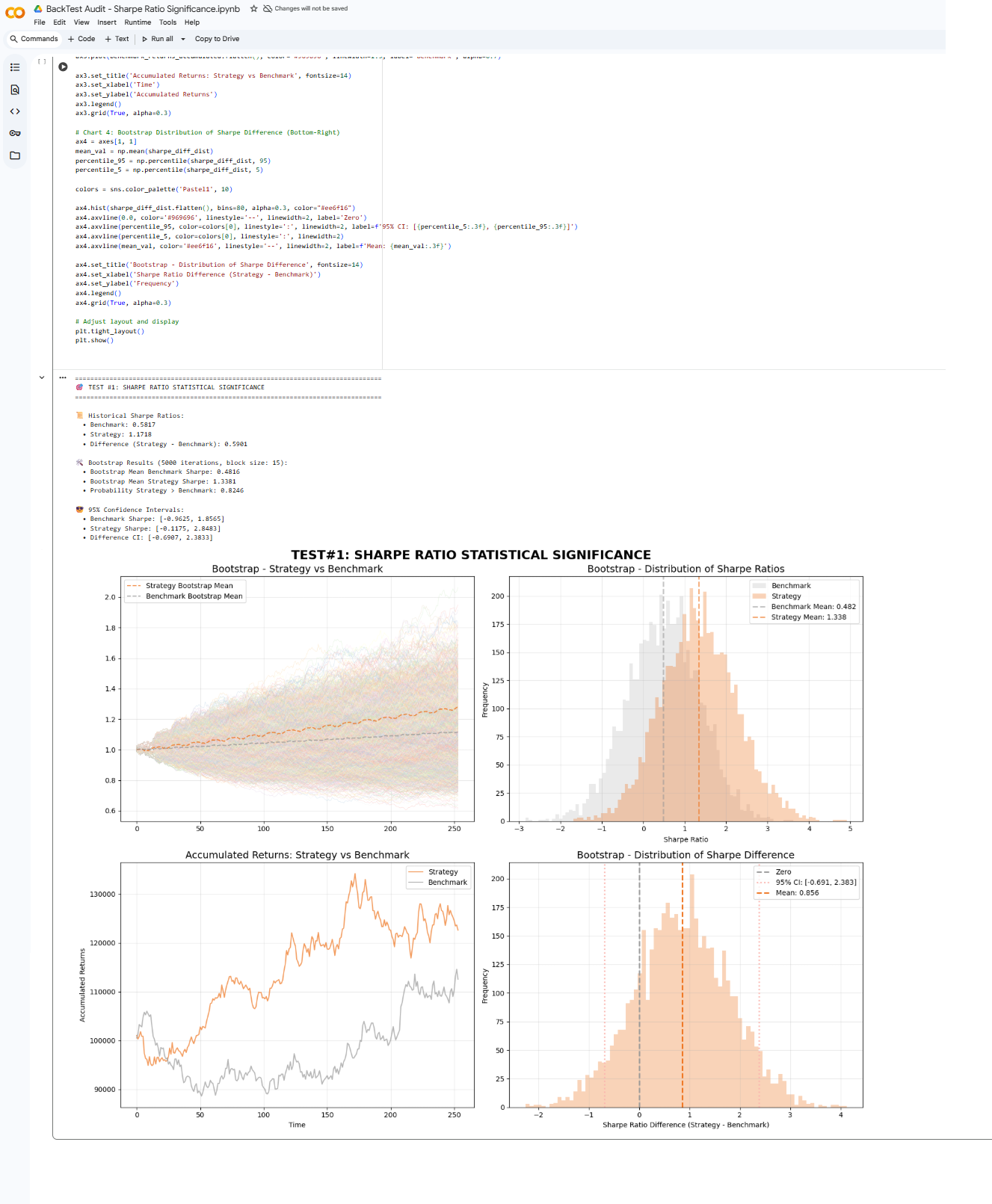

#1 - Sharpe Ratio Statistical Significance

The first test in my trading strategy validation framework is “Sharpe Ratio Statistical Significance” test.

🤔 Question To Answer:

Is the strategy’s Sharpe ratio really better than zero, or could it just be due to random chance, even considering unusual return patterns and time-related effects?

🔎 How?

Uses 5,000 block bootstrap iterations to preserve serial correlation in returns.

Calculates the Probabilistic Sharpe Ratio (PSR) by using bootstrap resampling i.e. repeatedly sampling from the data to create many possible scenarios and measure how often the Sharpe ratio stays above a certain level.

Conducts a Sharpe difference test comparing the strategy against the benchmark with 95% confidence intervals.

Applies the Ledoit-Wolf studentized time-series bootstrap for added robustness for 2nd opinion.

✅ Pass Criteria

The Probabilistic Sharpe Ratio (PSR) should be greater than 0.95.

Alternatively, Ledoit-Wolf test p-value should be less than 0.05 to indicate statistical significance.

This test essentially validates whether the strategy’s risk-adjusted returns are reliably positive and not a result of random chance or market artifacts.

(4 more simulation testing will be available SOON, stay tuned!)

(Disclaimer: The contents are for educational purposes only, sharing personal experiences and insights in developing and backtesting quantitative trading strategies using principles of quantitative finance. Developing or using quant trading strategies is a method or tool, not financial advice. The information provided, including coding techniques, backtesting methods, or statistical models, is general knowledge and not specific recommendations to buy or sell securities. It is not related to investment opportunities, passive income, debt relief, financial services, or financial consulting. I do not provide financial advice or services)

🚨 Stop wasting time for strategy in live testing that probably not going to work!

Unlock the exact code in this post to test validate your strategy before forward testing

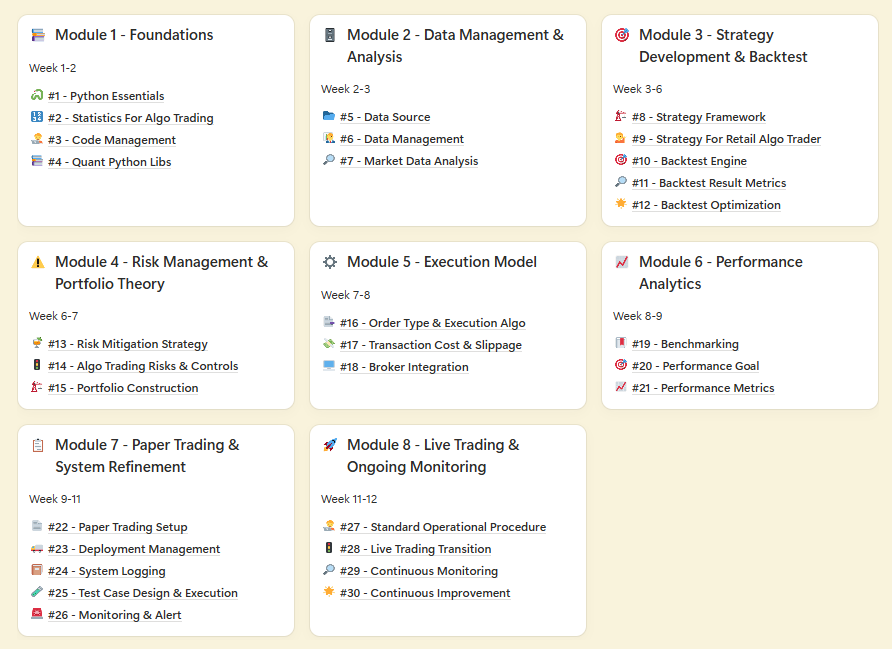

BONUS For Paid Member ONLY - “Champion’s Fast Lane Playbook: Master Algo Trading in 12 Weeks” - My 8 modules self-study guides and notes for building a winning strategy.

⬇️⬇️⬇️